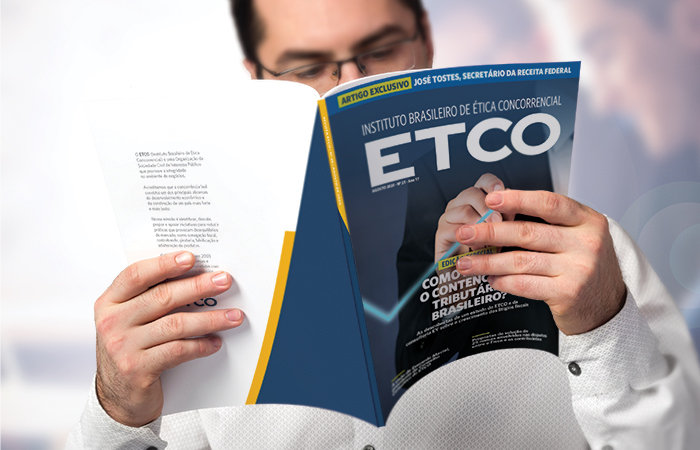

Contributions from 27 experts to resolve the tax litigation crisis

They debated the causes and solutions for the problem in a special issue of ETCO Magazine

Raising awareness in Brazilian society about the causes and losses of the high level of tax litigation in the country has been one of ETCO's priority projects. In 2019, the Institute hired the international consultancy EY to carry out a study on this important topic, which was presented to the public at the end of that year.

In 2020, among the initiatives that continued the work, one that stood out was the production of a special edition of the ETCO Magazine totally dedicated to the topic. Over several months, the publication heard 27 names involved in the litigation issue from different angles: taxpayer representatives, lawyers, tax authorities, tax auditors, attorneys from the National Treasury, Judiciary, non-governmental entities and economists.

The objective was to gather a wide range of views on the causes and proposed solutions to the problem.

The magazine featured an exclusive article by the secretary of the Federal Revenue, José Tostes, on the government's view of litigation and proposals to face it. He also published a long interview on the subject with tax expert Everardo Maciel, president of the ETCO Advisory Board, who was secretary of the Federal Revenue during the eight years of FHC's government. And it brought interviews with 25 prominent professionals in the business, legal, academic and three branches of government to portray the theme from different points of view.

Check out who the collaborators were and then the causes and solutions they pointed out:

WHO PARTICIPATED

José Tostes (1), secretary of the Internal Revenue Service; Everaldo Maciel (2), chairman of the ETCO Advisory Board; Adriana Gomes de Paula Rocha (3), from PGFN; Adriana Gomes Rêgo (4), president of Carf; Beno Suchodolski (5), tax expert; Breno Vasconcelos (6), tax expert; Cássio Borges (7), legal superintendent of the National Confederation of Industry (CNI); Hamilton Dias de Souza (8), tax expert and member of the ETCO Advisory Board; Helcio Honda (9), director of the Legal Department of the Federation of Industries of the State of São Paulo (Fiesp); Heleno Torres (10), Professor of Tax Law at USP; Juliana Araújo (11), from PGFN; Leonardo Alvim (12), from PGFN; Lorreine Messias (13), economist; Marco Bertaiolli (14), federal deputy; Marcos Lisboa (15), president of Insper; Mauro Silva (16), president of Unafisco; Nelson Machado (17), director of the Tax Citizenship Center (CCiF); Paulo Cesar Conrado (18), federal judge; Paulo Domingues (19), judge of the TRF-3; Phelippe Toledo Pires de Oliveira (20), from the PGFN; Raquel Novais (21), tax expert; Regina Helena Costa (22), minister of the STJ; Rita Bacchieri (23), vice president of Carf; Rita Dias Nolasco (24), PhD in Law from PUC-SP; Roberto Quiroga (25), tax expert; Vanessa Canado (26), tax specialist, special advisor to the Ministry of Economy; Zabetta Macarini Gorissen (27), executive director of the Applied Tax Studies Group (Getap).

The main causes pointed out

- COMPLEXITY OF THE TAX SYSTEM: The complexity stems from characteristics such as the fragmentation of the tax base and the right to legislate between the Union, the 27 states, the Federal District and the 5.571 municipalities in the country; unequal taxation by sector and product; and tax benefits.

- DELAY IN PACIFICATION OF JURISPRUDENCE: Judges and courts make different decisions for equal cases over many years until the issue is definitively analyzed by the higher courts.

- EXTENSION OF THE TAX PROCESS: A tax action can go through up to three instances in administrative bodies and another three in Justice – or four, if it involves a constitutional issue. And at each stage, different legal remedies are admitted.

- LOW QUALITY OF RULES: They are often created without taking into account international experience or the impacts they will have on taxpayer behavior. Many are poorly written.

- TAX ERRORS: They tend to assume bad faith on the part of all companies, without differentiating between involuntary errors of good taxpayers and attempts to deceive the tax authorities on the part of tax evaders.

- COMPANIES PROFIT FROM THE LITIGATION: In some cases, discussing the collection in court for years and then joining a refinancing program with a reduction in interest and fines brings a financial advantage to the company.

- EXCESS OF ACCESSORY OBLIGATIONS: In addition to calculating and paying taxes, taxpayers need to comply with a series of formalities and access different systems to send data to the tax authorities, which increases the risk of errors.

- TAX AWAY FROM TAXPAYERS: The agency is structured to look for errors, not to help taxpayers understand the law. Query solutions take too long, are too generic, or have a pro-fiscal bias.

- LITIGATION CULTURE IN THE COUNTRY: There is mutual distrust between taxpayers and the tax authorities and a predisposition to legalize conflicts.

The main suggested solutions

- EXPAND CONFLICT RESOLUTION MECHANISMS: Approving new or more using existing instruments to prevent and resolve conflicts individually. This group includes the tax transaction, the procedural legal business, mediation, conciliation and arbitration.

- CARRYING OUT A TAX REFORM: Simplifying taxes and reducing tax benefits and differential treatments that are at the root of many disputes between the tax authorities and taxpayers.

- BRINGING TAXES TO GOOD TAXPAYERS: Adopting criteria to differentiate good taxpayers from bad taxpayers. And the creation of tax compliance programs to facilitate the relationship between the tax authorities and the companies of the first group.

- FIGHTING THE CONTINUOUS DEBTOR: Establishing criteria to distinguish the occasional debtor from the persistent debtor of taxes, which structures its business to never pay taxes, distorting fair competition and harming the tax authorities in billions, as provided for in the Senate Bill No. 284, of 2017, which is shelved.

- RENEGOTIATING THE LITIGATION STOCK: Approving a realistic program for the regularization of tax debts that takes into account the financial capacity of taxpayers and rewards those who continue to pay.

- DEMAND QUICKER RESPONSES FROM SUPERIOR COURTS: Forcing the STJ and the STF to be more agile in the pacification of jurisprudence and in the resolution of conflicts of a constitutional nature involving many taxpayers.

- REFORM THE TAX PROCESS: Making changes in the way in which tax disputes are judged, such as reducing stages, reducing possibilities for resources and changing the roles of the judging bodies.

- ALLOW TAX SELF-REGULARIZATION: Authorizing the taxpayer to correct flaws identified in the inspection process without the need to apply a tax assessment notice.

- IMPROVE THE CREATION OF RULES: Establishing strict criteria for the approval of rules, such as exposing the reasons for their creation, detailing the purposes of each article and publishing their preparatory documents.